- Articles

- Insights

Explainer: What’s really driving natural gas prices?

June 10, 2026The U.S.–Iran war has ignited a period of elevated market volatility, particularly in energy markets. While most of the attention, at least in North America, has been on soaring oil prices, overseas, everyone’s talking about natural gas.

In Europe, natural gas prices surged by upwards of 70% on March 4th, as tanker traffic through the Strait of Hormuz ground to a halt. In Asia, prices shot up as much as 140% by mid-April. In North America? Nothing.

Unlike oil-focused traders, who have taken advantage of volatility, with prices climbing upwards of 25% on some days, natural gas flows haven’t offered that same opportunity closer to home.

Why not? We’ve put together a natural gas explainer to help you make sense of this market.

Why hasn’t the war impacted gas prices in North America?

Let’s start with the Strait. Roughly 20% of global liquified natural gas (LNG) (and also oil) flows through that narrow strip of water in the Middle East. None of that supply, though, finds its way to North America.

Wait, we don’t get any of the oil that comes through the Straight either.

You’re right about that, but oil is seen as much more of a global commodity, which means supply issues in one region often impact prices in another. Natural gas markets, though, are more local, with domestic supply pushing prices higher or lower.

In North America, and particularly in the U.S., the world’s top natural gas producer, advances in fracking technology and storage capacity have meant that domestic natural gas production has no problem meeting demand. (Canada’s producing natural gas at record levels, too.)

Saying all that, the gas disruptions facing countries in Europe and Asia are not impacting markets here, at least for now. Prices of Henry Hub, the benchmark for North American gas, are down about 7% since February 27 (as of April 29), the day before the conflict began, but they haven’t moved much over the past two months.

But I thought natural gas was a more volatile commodity than oil?

That’s right. Gas is one of the most volatile commodities around, and especially when compared to oil. If you look at this chart, which tracks the 90-day volatility of the two commodities, you can see that gas is more than twice as volatile as oil. (The 30-day volatility numbers show that oil has been more volatile than gas, driving the point home that North American gas has not been impacted by the war.)

What then is driving the price if not geopolitics? Good old weather. When it’s cold, demand for gas, which heats people’s homes, can spike, pushing prices higher. In a milder winter, demand drops, and so too do prices. It’s similar in the summer – if it’s too hot and everyone’s running their air conditioners, the need for gas can jump.

Look at the biggest spike in 2026. It was late January, when a brutal cold snap pushed deep into the Southern states, causing prices to climb by 63% to US$5.08 from US$3.08 in six days. While there were a few big ups and downs in the days that followed, a month later, gas prices were back to where they were before the temps plummeted.

That can’t be all that moves prices.

Nope. How much gas is stored – typically in underground facilities – can impact prices, too. If storage levels are high, there’s a lot of gas available, which can help absorb any supply shocks. During a cold snap, for instance, producers and utilities can draw from stored supply instead of scrambling to buy more at higher prices. That tends to keep prices stable.

When storage is low, the opposite happens. If demand spikes, the market has fewer options, and prices can rise quickly as buyers compete for the limited supply.

The level storage is important, but so too is how it compares to what’s typical. Traders often look at inventories relative to the five-year average. If storage is above that level, prices could face pressure. If it’s below, markets can get nervous, especially heading into winter, when demand is highest.

Storage also follows a seasonal rhythm. Gas is typically put into storage during the warmer months and withdrawn in the winter, which means people aren’t just reacting to how much gas is in storage today, but how quickly it’s being added or drawn down. Weekly storage reports can move prices on their own if the numbers come in higher or lower than expected.

All that’s to say, storage is one reason North American natural gas hasn’t reacted like global markets during the current conflict. With strong production and relatively healthy inventories, the system has been able to absorb external shocks.

Ok, so if someone is interested in trading a gas ETF, should they be concerned with what’s happening overseas?

No, not exactly. Longer term, America may not remain insulated from global gas shocks. Over the last decade, the U.S. has slowly expanded its LNG export market, shipping gas mostly to Europe and Asia. By connecting to the broader market, prices should, in theory, be impacted by global forces.

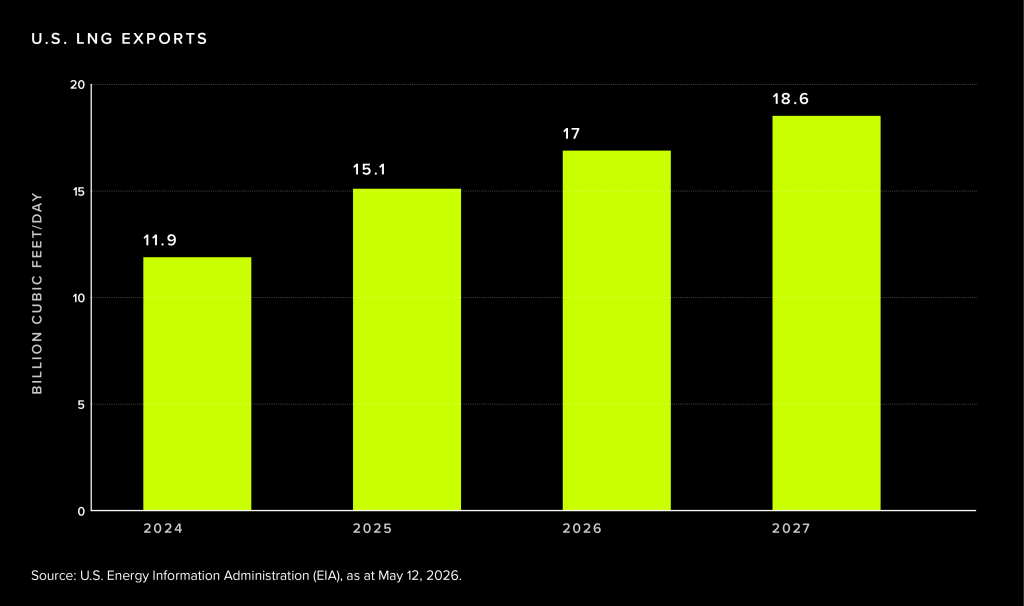

For now, though, exports are capped by liquefaction capacity, which means they can only ship so much. But a wave of new export projects is set to come online later this year, including Corpus Christi Stage 3, Golden Pass and Plaquemines, putting more U.S. gas into global markets. The U.S. Energy Information Administration (EIA) expects LNG exports to reach 18.6 billion cubic feet per day by 2027, a more than 50% increase from 2024 levels.

At the same time, inventories are expected to tighten, which could make gas prices even more volatile in the future. The EIA forecasts that by October 2027 storage levels could fall below the five-year average and reach their lowest levels since 2022, just as demand ramps up heading into winter.

Lots of moving parts here. What could this mean for someone interested in leveraged and inverse leveraged natural gas ETFs?

In the short term, North American natural gas remains a weather and storage trade, not a geopolitical one. Volatility is still tied to temperature forecasts, weekly storage reports, and how supply compares to seasonal norms, rather than to events overseas. So, for traders, watch forecast revisions closely, track storage versus the five-year average and pay attention to how quickly inventories are being built or drawn down.

That said, drivers may start to shift. As LNG export capacity expands and more U.S. gas is drawn into global markets, international price shocks could matter more. Over time, market participants may need to keep one eye on domestic fundamentals and the other on global LNG flows and export capacity.

Disclaimers

Commissions, management fees and expenses all may be associated with an investment in products (the “Global X Funds”) managed by Global X Investments Canada Inc. The Global X Funds are not guaranteed, their value changes frequently and past performance may not be repeated. Certain Global Funds may have exposure to leveraged and inverse leveraged investment techniques that magnify gains and losses which may result in greater volatility in value and could be subject to aggressive investment risk and price volatility risk. Such risks are described in the prospectus. The prospectus contains important detailed information about the ETF. Please read the relevant prospectus before investing.

The Global X Funds include our BetaPro products (the “BetaPro Products”). The BetaPro Products are alternative mutual funds within the meaning of National Instrument 81-102 Investment Funds and are permitted to use strategies generally prohibited by conventional mutual funds: the ability to invest more than 10% of their net asset value in securities of a single issuer, to employ leverage, and engage in short selling to a greater extent than is permitted in conventional mutual funds. While these strategies will only be used in accordance with the investment objectives and strategies of the BetaPro Products, during certain market conditions they may accelerate the risk that an investment in shares of a BetaPro Product decreases in value.

The BetaPro Products consist of our Daily Bull and Daily Bear ETFs (the “Leveraged and Inverse Leveraged ETFs”), Inverse ETFs (the “Inverse ETFs”), and our BetaPro S&P 500 VIX Short-Term Futures™ ETF (the “VIX ETF”) and can offer opportunities for enhanced returns or hedging strategies, but it’s essential to understand and accept the associated risks. Leveraged ETFs aim to amplify the returns of an underlying index, which can lead to higher gains, but they also magnify losses in downturns. Similarly, inverse ETFs seek to profit from declines in the underlying index, meaning they can perform inversely to the market, but losses can accumulate quickly if the market moves against expectations. While these strategies will only be used in accordance with the investment objectives and strategies of the BetaPro Products, during certain market conditions they may accelerate the risk that an investment in shares of a BetaPro Product decreases in value. Investors should be aware of and understand their risk tolerance and capacity, and conduct their research before investing. An investment in any of the BetaPro Products is not intended as a complete investment program and is appropriate only for investors who have the capacity to absorb a loss of some or all of their investment. Please read the full risk disclosure in the prospectus before investing. Investors should monitor their holdings in BetaPro Products and their performance at least as frequently as daily to ensure such investment(s) remain consistent with their investment strategies.

Certain statements may constitute a forward-looking statement, including those identified by the expression “expect” and similar expressions (including grammatical variations thereof). The forward-looking statements are not historical facts but reflect the author’s current expectations regarding future results or events. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results or events to differ materially from current expectations. These and other factors should be considered carefully and readers should not place undue reliance on such forward-looking statements. These forward-looking statements are made as of the date hereof and the authors do not undertake to update any forward-looking statement that is contained herein, whether as a result of new information, future events or otherwise, unless required by applicable law.

This communication is intended for informational purposes only and does not constitute an offer to sell or the solicitation of an offer to purchase investment products (the “Global X Funds”) managed by Global X Investments Canada Inc. and is not, and should not be construed as, investment, tax, legal or accounting advice, and should not be relied upon in that regard. Individuals should seek the advice of professionals, as appropriate, regarding any particular investment. Investors should consult their professional advisors prior to implementing any changes to their investment strategies. These investments may not be suitable to the circumstances of an investor.

All comments, opinions and views expressed are generally based on information available as of the date of publication and should not be considered as advice to purchase or to sell mentioned securities. Before making any investment decision, please consult your investment advisor or advisors.

Global X Investments Canada Inc. (“Global X”) is a wholly owned subsidiary of Mirae Asset Global Investments Co., Ltd. (“Mirae Asset”), the Korea-based asset management entity of Mirae Asset Financial Group. Global X is a corporation existing under the laws of Canada and is the manager, investment manager and trustee of the Global X Funds.

© 2026 Global X Investments Canada Inc. All Rights Reserved.

Published June 10, 2026

Related Articles